Listen:

Check out all episodes on the My Favorite Mistake main page.

My guest for Episode #202 of the My Favorite Mistake podcast is Shaun Hayes. He was the cofounder and former CEO of Allegiant Bancorp, headquartered in St. Louis, Missouri. Shaun started multiple successful businesses, was involved in the casino business, and bought, owned, and sold hundreds of residential and commercial properties. He is an entrepreneur, an author, a speaker… and a felon.

He was a principal at three banks that failed in 2011 and 2012. Five years after selling a company for an enormous profit, Shaun committed a felony. He was incarcerated for his crime eight years later. Now out of prison, he’s the author of The Gray Choice: Lessons on My Journey from Big-Time Banking to the Big House (and Back).

In this episode, Shaun tells two favorite mistake stories. The first was about “going crazy and wanting to fire somebody” when he then realized that the problems were the result of his mistakes as CEO of the bank. The second story is about the mistakes and bad choices that led to his conviction.

Shaun discusses the impact of his experience on his personal and professional life and how he has worked to rebuild his reputation and move forward. The episode offers valuable insights into the challenges of entrepreneurship and the importance of taking responsibility for one's actions.

Shaun provides valuable insights into the challenges of entrepreneurship, discussing how his ambition and drive to succeed led him down a path that ultimately resulted in his downfall. He emphasizes the importance of taking responsibility for one's actions and not making excuses, acknowledging that he made mistakes and accepting the consequences of his actions. Despite the difficulties he faced, Shaun remains optimistic and determined to use his experience to help others learn from his mistakes.

We also discuss the challenges of being a CEO, the importance of transparency and honesty in business, and the need for forgiveness and second chances.

Questions and Topics:

- At an early age – making decisions that are not illegal but grey in the “interpretation of the rules”?

- How he justified it…

- Why go forward with it even knowing it was illegal?

- Did this lead to bank failures?

- Why did the legal process take 7.5 years to play out before being indicted?

- The dynamics / decision around pleading guilty?

- Do you remember something early on that got you 1% off course?

- The need to specifically define your moral compass?

- What’s it like starting a business once out of prison?

- Being a speaker today to help others?

Find Shaun on Social Media:

Watch the Full Episode:

Quotes:

!["I wanted to fire someone [for that mistake]. And by the end of the week, I went back to my management team and I said, 'I figured out who it is —

it's me.'" SHAUN HAYES](https://www.markgraban.com/wp-content/uploads/2023/03/Shaun-Hayes-My-Favorite-Mistake-Quotes-1.jpg)

Subscribe, Follow, Support, Rate, and Review!

Please follow, rate, and review via Apple Podcasts or Podchaser or your favorite app — that helps others find this content and you'll be sure to get future episodes as they are released weekly. You can also become a financial supporter of the show through Anchor.fm.

You can now sign up to get new episodes via email, to make sure you don't miss an episode.

This podcast is part of the Lean Communicators network.

Other Ways to Subscribe or Follow — Apps & Email

A Former Bank CEO's Journey From Entrepreneurship To Incarceration And Back: Shaun Hayes

A quick note. I recorded this episode with Shaun Hayes on February 21, 2023. We're going to be talking about some bank failures in the past, and this was recorded before banks started failing here in the US. That's why we don't address any of that in terms of current events, but I think you'll still find his perspective interesting and helpful. Thanks.

—

This is episode 202 with Shaun Hayes, author of the book The Gray Choice. In this show, you'll hear business leaders and other really interesting people talking about their favorite mistakes because we all make mistakes. What matters is learning from our mistakes instead of repeating them over and over again. This is the place for honest reflection and conversation, personal growth, and professional success. Visit our website at MyFavoriteMistakePodcast.com. To learn more about Shaun Hayes, his book, and more, go to MarkGraban.com/Mistake202. As always, thanks for tuning in.

—

Our guest is Shaun Hayes. He was the Cofounder and former CEO of Allegiant Bancorp, which was headquartered in St. Louis. Shaun started multiple successful businesses. He was involved in things including the casino business. He bought, owned, and sold hundreds of residential and commercial properties. He's an entrepreneur, an author, a speaker, and a felon.

You don't always expect to see that at the end of someone's list of labels or titles, but I appreciate that Shaun is willing to talk with us. He's the author of the book The Gray Choice: Lessons on My Journey from Big-Time Banking to the Big House (and Back). He is joining us as part of his end-back journey. We're going to have a lot to talk about. Shaun, thank you for joining and being with us. How are you?

I'm wonderful, Mark. Thank you for having me. I look forward to this.

The title of the book, I don't know if it’s a little bit about your story there, but it probably doesn't ruin your story. I don't know which story you consider to be your favorite mistake. I think we have two stories here. What's the first favorite mistake story that you'd like to share, Shaun?

We started in ’89 and I bought my partner in ’92. Many of your audience who have been business for themselves can relate to this, but if they have anything to know about banking, it's hard for banks to realize. In nine years, we grew 50-fold. That's unheard of. Along the way, one of the key things I learned, and I think this goes across all businesses, is that IT is for the little guy because you have big investments in systems. There are a lot of off-the-shelf things you can do that solve problems. We brought in an IT guy in ‘93 after I'd failed at buying the bank he was with. Things were unbelievable the next years. We did things that the big banks couldn't do.

In 1995, he had personal issues and said, “I'm moving to Florida. My lieutenant can hold this together for about a year but you need to find someone.” The long and the short of it was, he was right. The good news is we found a woman who I think walks on water. The bad news is it took a whole year. She got there in August and I said, “Kim, we're going to do whatever you want to do because I saw what Jim was able to do for us over about two and a half years. I trust you.” She came back in about six weeks and said, “We need to do this.” For us, it was a $1.7 million investment, which was a lot of money.

This was in November and she said, “It'll be done the next November.” I said, “Okay.” I went to the board about two weeks later and we approved it. In my mind, it's solved. Being an entrepreneur, here's where my mistake kicks in. She said, “There's one thing, Shaun. You can't buy another bank between now and next November.” Mark, that went in this ear and out the other ear. In March, I got a chance to buy one. She said, “Shaun, you can't do that.”

Why was she saying that? Would it cause problems with the IT implementation?

This is what I didn't realize until we got to September. This is when I learned my lesson and it truly was a mistake. When I tell you the mathematical error in it, you'll get the magnitude. What she was saying was, first, we're buying all this hardware and software. Second, we have to train people for months, then it takes weeks to install it, train them, and use it, and then we turn it all on. My mind is you went to the store, you bought a program, you came home, you popped it into your computer, and a few hours later, you were playing ball. It didn't work that way. In March when I bought this bank, I said, “Kim, no problem. Here's what we'll do. I won't merge it in until next March.” It’s because it was small. It was only $30 million.

It was about 20% of our size at that time. That calmed her down and we made it through that. When we get to May and in St. Louis, what's now US Bank made big acquisitions of savings and loans. The Federal Trade Commission made them divest. We were a $600 million bank and we were borrowing $100 million overnight, which is not a good resolution for a business. It'd be like a company saying, “I need a six to my balance sheet and I want it on demand,” meaning the bank can agree not to renew it the next day. All of a sudden, I could buy $100 million in deposits and the price was right.

It was two markets we weren't in. Kim said, “Shaun, it's going to be a problem.” She had only been there about 8 or 9 months. She didn't really have the ability to communicate the level of magnitude of a problem. As an entrepreneur, a problem is no problem. We signed a contract and the announcement came Memorial Day weekend. We had to close Labor Day weekend. On Labor Day weekend, I go to all these banks. We have a great zoo in St. Louis for people who have never been here. It's one of the best in the world. I take my kids to the zoo and my debit card doesn't work. It doesn't resonate and it’s no big deal. By the time I got by Tuesday, a bank in those days would close at 2:00 and then start a new day.

What that meant was is you started processing. We were considered a large bank then. Not a huge bank like we became now. We would start processing at 2:00 and we'd be done around 7:00. These banks had so many transaction accounts. They took us from 2:00 until noon the next day to process. This is going on and by the middle of that week, we figured out that if you went to a bank and cash a check at our bank or if you went to one of our ATMs, we didn't capture it. There was no what's called on-us. Therein lies a mistake and I had all kinds of people who called me up the month later and said, “Shaun, I got $250 and you never charged my account.”

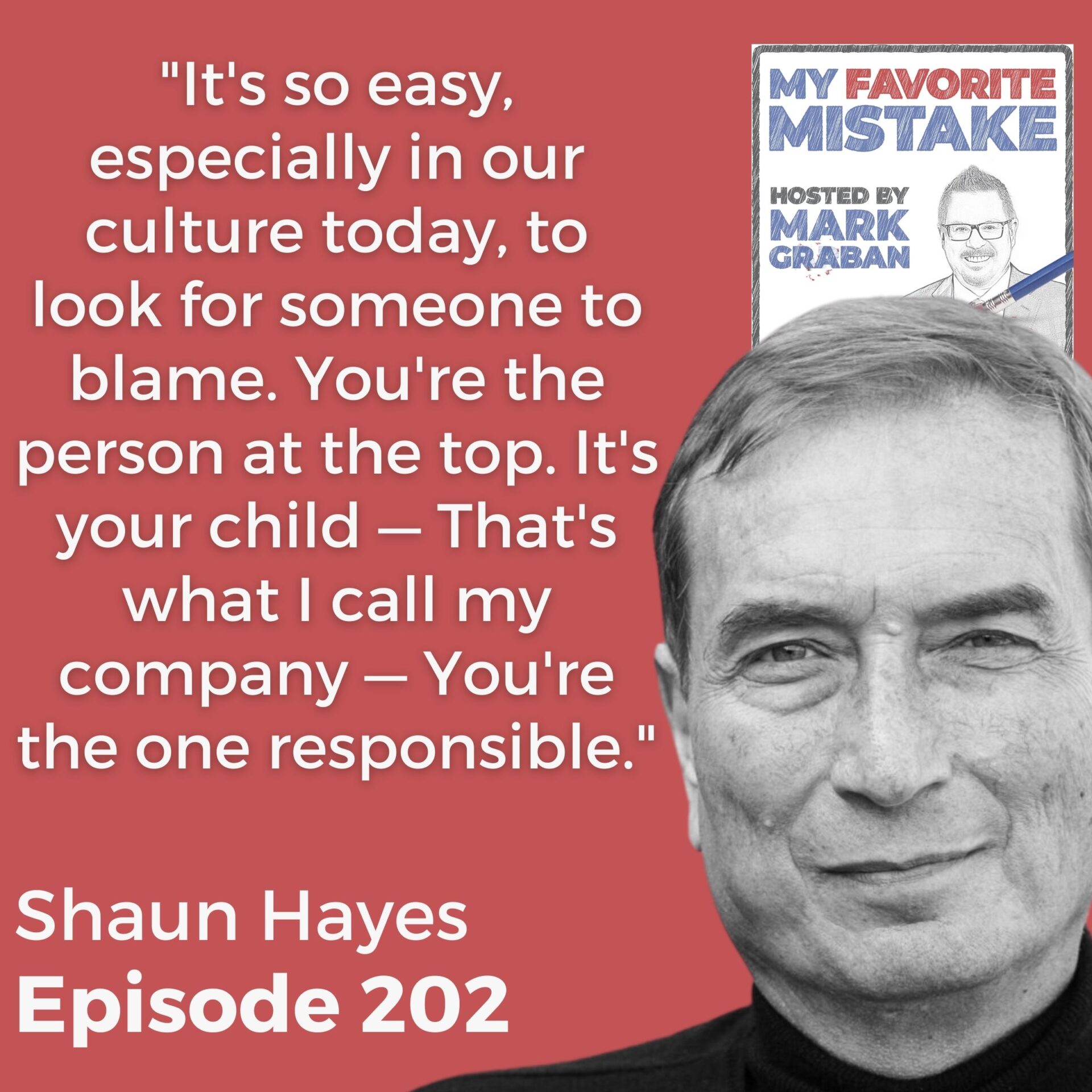

$1,547,000 walked out the door that weekend that we couldn't find. Two pieces of that and then I'll get to the mistake that I found. One, that year, we made about $6 million after tax. It was about 15% or 16% of our after-tax earnings. Our earnings are public. We’re up over 20% that year but no one noticed it. If you read the annual report, it was still buried in the footnotes, but I'll never forget $1,547,000. The lesson in it and the mistake was, that week, I wanted to fire someone. I went crazy. I didn't mention Kim managed to have a child during this period. We had to set up in a hospital room a computer system.

That whole week, I'm screaming, “We have to fire someone. We have to hold someone accountable.” By the end of the week, I went back to my management team and I said, “I figured out who it is. It's me.” When you say your mistake, “It was my mistake not to listen and understand. It was my mistake to buy this as an important acquisition and all this rested on me.” It's so easy, especially in our culture now to look for someone to blame. I learned that at the end of the day, you're the person at the top. It's your child. That's what I call my company. You're the one responsible. That was an unbelievable lesson in making a very expensive mistake because three years before, we didn't make $1,547,000 pre-tax. It was the magnitude of the loss and it was how quick it disappeared.

I wanted to fire someone for that mistake. And by the end of the week, I went back to my management team and said, 'I figured out who it is—it’s me.' Share on XWhat it did was it sucked the life out of our culture for about a year. We were a different company. What we did in that year was we made a lot of tough decisions. We consolidated. We did some things that we would never have done. I would say you always have to remember it. I think Harry Truman had the thing on his desk, “The buck stops here. It stops with the CEO.” That's the one lesson. The other lesson is, when you make a mistake like that, what can you do with it? In our case, we sold some things that didn't fit. We spun some businesses off. We did things and we didn't grow for one year, which was ironic for us as much as we grew in that nine-year span. We made more money and we were a better company. Good came from it but the mistake was horrific.

That's a great story. I appreciate you sharing the reflections and the lessons learned from that. Did somebody have to talk you out of firing somebody that week?

I had seven great direct reports. The one that run HR was unbelievable. The whole time, I had someone I wanted to fire because, to me, it rested on the man that oversaw the processing. How could it take 20 hours with a new system when it should have taken 2 or 3 and not 5 or 6 even because we weren't using it even more near the capacity? She and Kim were close. Kim was in the hospital this whole week period having a newborn with her. Karen was able to communicate with me.

She was like, “Shaun, this man was executing your orders, doing your job in a chain of command. You know that there could be consequences. I love that about you and our culture. If you do something right, we recognize it. If you do something wrong, we don't necessarily fire you, but we hold you accountable. You got to look in the mirror.”

She'd been there longer than Kim. She had to look me in the eye and say that. That's another point I'll make. I would say I believe every business is its people. I said, “For years, my HR people could interview you,” and they would say, “You're going to love these seven things and you're not going to like these too but he's really going to fit in our culture. He's going to be a high performer, but you, Shaun, have to adjust your style to those two.” Meaning I'm not going to change but I had to adapt. She had my ear in that way and she saved Mike's job because, left off my own devices, I would've fired him by Friday. I was so darn angry.

It’s so easy, especially in our culture today, to look for someone to blame. You’re the person at the top. It’s your child—that’s what I call my company—and you’re the one responsible. Share on XAt least you listened to the HR person. I appreciate you mentioning you're not blaming Kim for not convincing you of the level of magnitude, the risk, or the problem. As you said, you found the problem in the mirror and you took responsibility for it. How did that affect the way you handled other situations going forward as a CEO?

It humbled me. One, you like to believe you're perfect and yet we know we're not. It was humbling to have to go back, especially to the seven people that I spent so much time with because I was on a tangent of someone had to serve a consequence for that, and I didn't. It made me more cognizant of my decision-making. We're going to talk about my next mistake in a little bit and you're going to see by then, I had forgotten my lesson. As many of us, especially back to our culture now, we have short memories. Whenever we have short memories, we pay a price. I pay a much greater price for my next mistake.

Before we get to that, I have one other comment I was going to make. You talk about the tendency to blame. I don't think that's even a modern society thing. It's almost more human nature. You could look at it from an evolutionary standpoint. There's an old story I'll tell quickly about Koko, the gorilla. The handlers, for lack of a better word, had taught Koko American sign language. There's a famous story that Koko had a pet cat, like a real live living cat. Koko was taught to do these things and loved the cat.

One day, the handlers came back and saw a sink had been torn out of the wall. It was clear that Koko had done this and they asked Koko. Koko supposedly in sign language replied, “Cat did it,” which of course, Koko didn't get away with that lie. I think something is very human nature. I could see where it's a survival technique, even if it's a matter of corporate survival. If you can blame someone else, I could see why we would have a tendency to try that.

It has been around 10,000 years, but it seems more prevalent now because we live in a society that's become more victim-oriented.

That's a different dynamic. It’s a more modern-day dynamic. I didn't want to sidetrack you, Shaun, from the second story. I think I know what it is. I could be wrong but let me tee you up to talk about this other favorite mistake.

I know you've heard this but there's a saying that seldom in life are your greatest dreams and realized are your worst fears. I'm going to say that I certainly have had both. I never thought I would start a company, take it public, have unbelievable success, and sell it at the pinnacle of the industry's height in sales. At the same time, I never thought I would go to prison. In my mind, the only thing that worst could happen would be losing a child. I can't think of anything better that could have happened in my career since I've done both. I think the segue I would use into this is the title of the book is a great choice. I won't tell the story but I'll tell the example because there's a story similar to my personal experience.

If you leave Los Angeles on a plane headed for Washington, DC and you're off by one degree given time, speed, and distance, you end up in New York City. I started at an early age in my career by making decisions that were not illegal or not criminally illegal. I told my lawyers this and this is what got me in trouble, and I did it to myself absolutely. It was, “Don't ever tell me I can't do something. Tell me how I can do what I want to do.” The example is, if I'm in St. Louis, it'd be logical for me to take Vanderbilt Avenue, get on Highway 64, and take 55 to Chicago. That's a simple way or I could go to the airport and take a flight in. My lawyers might say, “No, you have to take I-70 to Kansas City, 35 to Des Moines, hitchhike to Minneapolis, and ride the train to Chicago.”

I would be left with a decision. Do I want that much time and that much money in my effort to get to Chicago? I can do it. That was the culture that I instilled in myself and my company. We pushed and we would get legal advice on how to interpret how to do things. Once you start doing that, what happens is this. You have in your mind that 1) You become successful so you think you can do anything. 2) Because you're seeking an answer that's going to let you do what you want to do, you now think you can do about anything. Someone asked me a question, not on a show like yours, but they asked me. I said, “You don't wake up that there are people that are wired that will do something criminal.”

It took me many years of operating like that. What happened to me was when the recession hit in the collapse in ‘08, I was losing tens of millions of dollars a month personally. What I didn't realize, and it's pretty obvious when you look back, was all my investments were in banking, financials, and real estate and real estate collapsed. What went down with real estate is finances. I'm literally bleeding to death at the rate of $10 million a month. I went out to recreate what I'd done before and I had a way of doing it. That part was sound I'll say then we'll get to where I got off course. What I'd lost, and these are back to your audience, is when you're entrepreneurial and you're doing it, you have your ear to the ground.

I call it guerrilla warfare. You're very basic and tactical. You have great market intelligence. Why spend four years with a Fortune 200 as one of the top 35 people out of 36,000? I had lost four years of market. Not only did I lose four years of market intelligence, but I also lost it when the world changed when the subprime ended. It’s not an excuse, but the reality is that I'm out of touch with it. What had worked so well for me for 15 to 20 years before didn't work any longer. This is back into your audience, especially if you have a business for yourself. Surround yourself with bright people. I talked about the seven people who worked for me but I had a board of directors in particular and then there were four other people that we met a couple of times a month for fifteen years.

They helped me with a level of accountability. They made me successful because they were the kind of people that none of them had any banking experience. They would say, “Why do you do what you do the way you do it?” When they asked that question, the answer is, “Better not be because we've always done it that way.” That meant we had to retool. That's how bright these people were. They were all 15 or 30 years older than I was. They were either dying or retiring so I lost a group around me. I lost my own market intelligence. Since I was losing so much money, I didn't use good professionals. I'm not making excuses. At the end of the day, I made the decisions I made. The point is and the mistake here is when you lose those three things, those are crucial to anyone's success in business.

Quite honestly, the same elements are key in personal relationships in life. My backs to the wall are left to my own devices. This is how I justified it. 1) I had been successful in my decisions. 2) I had skirted out there with good legal advice, and obviously not this time because they wouldn't let me do something criminal. Thirdly is because I wasn't taking money. This was my justification. I'm not taking money. I'm manipulating documents to buy myself time because I know given time in my prior experience, I'll make this right. I committed a crime.

What was the crime? I don't know enough about this world. When you described manipulating the situation, that sounds bad, but maybe not illegal.

I own 54% of this bank. When you own more than 25%, you cannot do business with yourself on any terms. Less than 25% down to 5%, you should be to 10th of 1% or 1 share, you need to disclose it. Not only did I not disclose it, but I also couldn't do it to begin with.

This was a matter of loans “self-dealing.”

Self-dealing would be a much better term. Even though they knew I committed a crime, when I finally pleaded guilty, they brought a room full of accountants and forensic people and said, “Would you please tell us what you did? How did you do this?” What I'd done was I had watched a man in the late ‘80s, and we did this as a bank to a much smaller degree, I take banks and buy assets that were nonperforming. In those days, it’s as a resolution, trust, and other banks. The government doesn't like that.

They want you to only make loans that are good when you make them and you were making loans that were bad when you made them. I went to the trouble with a gentleman that I've known for many years. The irony in this is I knew this even before I did. I had described him. His brother was my securities lawyer, the largest firm in St. Louis. In his world, I described Tom as, “His world is 50% Black and 50% White. There is no gray. His brother, I would say had 1% Black and 1% White, and 98% gray from light to dark.” I knew what I was getting into, but he had hundreds of millions of dollars of loans that were nonperforming. I saw an opportunity to buy in.

I made him get other borrowers that could pay the debt. One was a doctor, a real estate guy, and a car dealer. You weren't relying on them because that made my argument. I'd watched a man do this and make hundreds of millions of dollars twenty years before. The problem was he and I had a loan at one of the banks that I was buying it from. In that loan, they wanted to get rid of everything to do with him. To facilitate the transaction and let me buy his debt or my bank buy his debt for $0.50 on the dollar, we had to buy a loan that I own half of. The loan was already out there but I didn't disclose in that package that I was on that loan. Therein is a crime and I knew it.

Why go forward with that then at the moment?

It’s because the transaction was so lucrative for us that we were making over $1 million-plus like that. That really made things better. Remember, I own 54% of this and I'm personally struggling at this point. The thing was I had watched this man do this for years on what he was going to do. Therein lies another mistake. I learned that people don't always want things as bad as you want them. It's my mistake, not his. I didn't realize the depth of his problems at that time. This was the $16 million in debt we bought was about a 10th of his problem.

What he did was, as soon as we bought them, he didn't do anything where the twenty years I'd done business with him before, he worked through them because he was incentivized to the seven-digit number. Forget the savings on the debt, but he had that much to earn in getting these properties sold and leased and all these things. That's how the other men made their money. He saw it as 1/10th of his problems were solved. Not only did I commit a crime and make a mistake there, but I made a mistake and a lesson.

Another lesson I learned was don't assume the other person wants something as bad as you do or has the desire to see something in completion. All this lie on me because I knew the day I did it, I'd committed a crime. The thing was, and this is again how I justified it, I wouldn't get any money. If he'd done what I'd watched him do twenty years, I'd known him before that. The ten years before he'd done that in business, it would've self-liquidated or disappeared. No one would've ever known. It would've passed, but I didn't do the right thing. I commit the crime right off the bat.

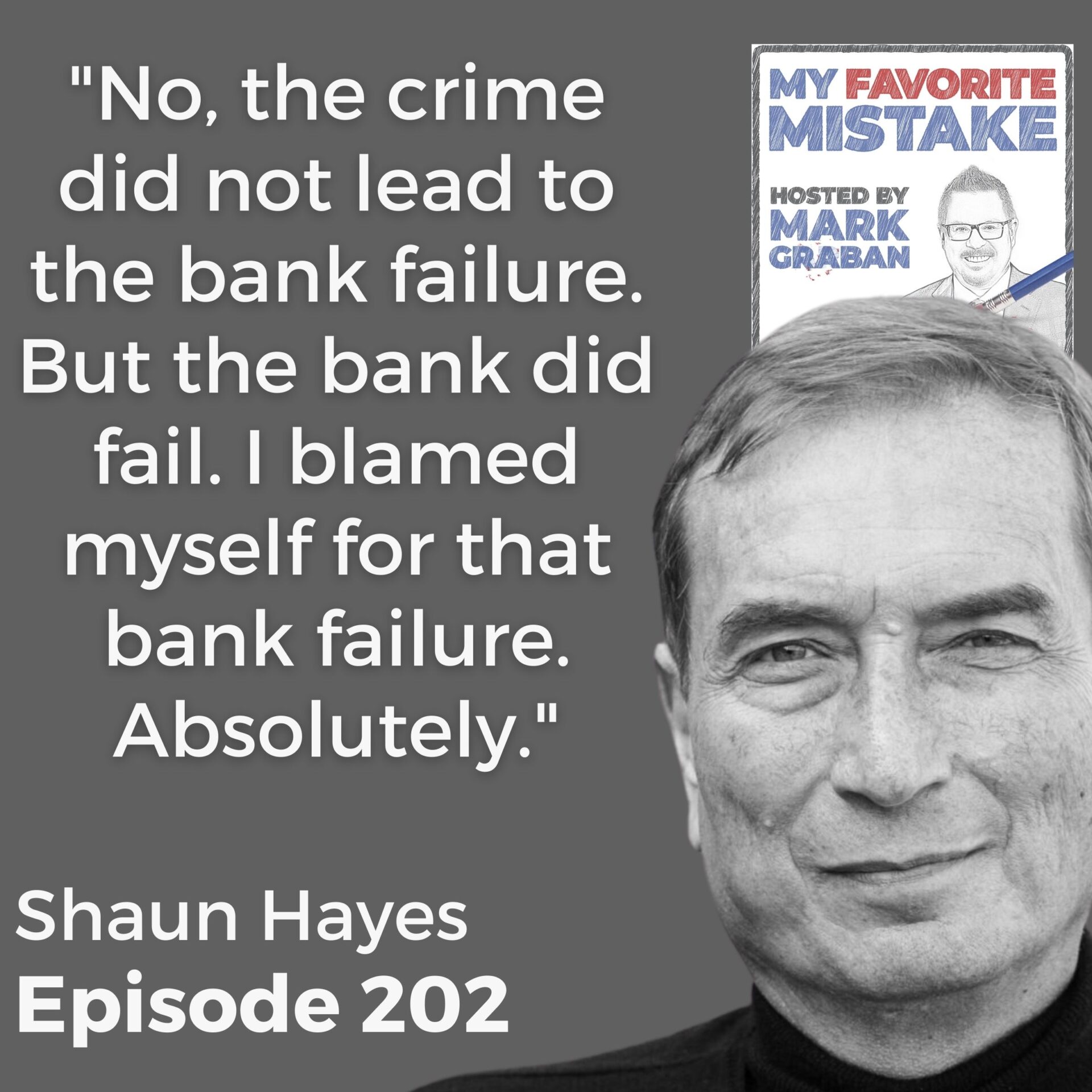

Did that crime lead to bank failure, or were there other factors leading to that?

No, the crime did not lead to the bank's failure but the bank did fail. It had problems when I bought it back to ground intelligence, but I contributed as a failure. That would've been a piece and a whole lot of other things like the lack of market intelligence. I blame myself for that bank failure. The crime in itself wasn't, but because the bank failed, there was a real forensic audit. It's like I described years ago. It's not like when somebody robs a 7-Eleven or a quick trip where they go in and then they call the police. They go get them and they try to get and find them immediately.

The crime did not lead to the bank failure, but the bank did fail. I blamed myself for that bank failure. Absolutely. Share on XThat happened on August 31st, 2009. I was questioned in 2013. I had a good bankruptcy lawyer friend that I'd done business for years. I had contacts in his attorney's office. He goes, “They passed on you at the end of September of 2013. Right at the end of 2015, they were on this other man for a whole lot of other reasons.” When they did forensics, I was a much juicier target than I should have been. I was in a position that I broke trust and I was in a position of trust. I broke the rules and the law. I paid a terrific price that I wouldn't want anyone to have to do.

This took years then it sounds like from getting the attention of law enforcement to the point of pleading guilty. Did you go through waves where you thought, “This isn't going to lead to criminal prosecution?”

Yes. It first came out in 2012 and then by the end of 2013, they said, “We can't find anything.” It came back up at the end of 2015. From the time I committed the crime until I got indicted was almost seven years. It was seven and a half almost eight years before I served a day. The consequence of that in itself is another cost. I deserve everything I got but it's what I did to my family, in particular to my marriage. I only owned 54% so I hurt other shareholders. Almost all of whom I think were employees. I betrayed their trust too. The damage I did was horrific. The lesson I learned there is, until that happened, I seldom thought of the law of unintended consequences. The unintended consequences of my crime were far. I threw a boulder into a pond. It wasn't a pebble.

Can you talk about the dynamics of deciding to plead guilty? You were sentenced to 68 months in Federal prison.

They first indicted me on 3 counts, and then about 10 months later, they expanded it to 10. As my attorney said, “You've been charged with the same thing ten different ways.” The way the system works, and I hope none of your audience has to figure this out for themselves, is they want to charge you to where if one thing doesn't work, but a slice of paper next to it does, they've got you. Quite honestly, as I described, my crime was so complicated. If I could have had my trial bifurcated from my co-defendant, I would've gone to trial. He says, “I don't think the jury can convict you of something that they can't describe as prosecutors in the average man or woman isn't going to understand.” What happened was and the reason that drove me in December of 2017, I lost a motion to bifurcate my trial.

The co-defendant had a business that I had nothing to do with. I wasn't involved in but he had done carry-back mortgages for people for 212 families. He didn't pay the first. He took their money. I would've been sitting at a table for weeks. They said, “We're going to bring in 212 families and talk about how they lost their homes.” At that point, the jury doesn't care whether you owned or did anything. You're sitting at the same table. My lawyer said, “You're going to get twenty years. That's going to be the consequence.” Once we lost that, I knew it was over.

Shaun, you talk about the idea of getting 1% off course, things that were in the gray area, and not illegal. Do you remember one of those early moments or decisions would've been?

In the early ‘90s, the Fed came out with a regulation that constrained real estate lending that was a derivative of the savings and loan collapse of the mid-late ‘80s and early ‘90s. I went to my attorneys because we had a niché that we lent money on. We owned a market for foreclosures, short sales, and tax sales. The niché in that was the sales were at noon in St. Louis City county and you had to have the money there by 2:00. Most people that played in that market didn't have the money to do that. If you wanted to buy a $100,000 house, you had to have $100,000. You had to have it there in less than two hours.

We'd set up a department that did that. At that time, we probably had $20 million or $30 million and before we were sold, we had $100 million. We charged huge fees and high-interest rates because we could. I went to the attorneys, and I said, “This is a niché.” They spent a lot of time and good money and said, “Here's how we believe you can legally comply.” They had to say believe because it was a new law. It was an interpretation. Sure enough, the government came in for the next ten years after that and we passed with flying colors. We created a system within our law that was totally in the gray. The irony in it was part of it was we track things, and if we lend you $100,000 to buy a house, we did you a six-month loan.

The average duration was about 92 or 93 days. Virtually in every case, if they didn't sell it, they went to another bank, and the other bank let them $120,000, $150,000, or $160,000 on what we'd let them $100,000 off. We were able to statistically prove that we were in compliance. We just couldn't comply given the timelines. That's that one step. Notice I had good counsel and good people. I did all the things I should have done because there's a lot of money in business in the margins or the gray. If you don't do it right, it's very easy to go from that step to the next step to the next step. Somebody sent me an email that had read the book and had known me many years ago.

He said, “Shaun, I now see how you got to where you got.” Not that I'm justifying it, but when everything is going against you in your back and hits the wall, your judgment gets clouded. We start justifying it like we were talking earlier about blaming people. Whenever everything is against you and you're there, it's a lot easier to say, “If I do this, I let my moral compass go. It's all on me.”

We're joined again by Shaun Hayes. The book is The Gray Choice: Lessons on My Journey from Big-Time Banking to the Big House (and Back). Before we wrap up, let's talk about some of the end-back story. You're out of prison and now you're doing other things. Part of what you're sharing with people is around this phrase. You use a moral compass and the need to define your moral compass. I guess it’s to help any of us not get 1% off track. Can you share a little bit more about how we might go about defining that compass?

I want to say two things there. I was reading the interviews and there was a lawyer that I knew tangentially going down almost 40 years. He used that quote when he was talking to the FBI. He said, “Shaun lost his moral compass,” and he was right. He hit the nail on the head. Secondly, something that I like to remind people is there was a study done by a Stanford professor years ago. The sum and substance of it was given the right set of facts and circumstances, any person can commit any crime. None of us like to think we could kill somebody, but he proved that point. I go back to the things that I said when I was looking at my own things. Surround yourself with people that are going to hold you accountable. If left at our own devices, we can do some pretty horrible things.

I don't even mean criminal things. That's one. Two is don't take your eye off the ball. I wouldn't change one thing because if I changed one thing, I wouldn't be in this position. I believe my mission is to help people not end up with what I did. I didn't have a plan after I reached the mountain. That was a mistake. I'm a big believer in planning. I'm a huge believer in goal setting. Once I reached them, I didn't have any. I was lost. That’s a big thing I always said to people and I knew this inherently, but I didn't apply it to myself. When you sell a business, it's like a death.

It's like a divorce. It's a whole thing. You have to have something else you're going to do. You should be thinking that long before you sell it. Those are the things if you surround yourself with good people. The sad thing for me was, even though I mentioned that the men and women who held me accountable for those 15 years were 15 to 30 years older. I had other people around me I could have gone to but then again, left to my own devices, I chose not to.

Restarting things, you're released from prison. What is it like trying to start a business and start working for others to help others? You've written a book. You're working to make a living. What have you experienced in this next phase of business and life?

One, I'm not complaining, but I now understand why the system is broken from being in the system and now being out and still in the system. I wanted to write a book and I wanted to speak. I was looking for a job because you're required to have one. The government wants you to have a 30-hour paycheck job. That's a requirement of every felon. I wanted to make beds in the largest hospital system in the metropolitan area. It employs some 20,000 people. They were so excited. I told them I was a felon and then they came back and said, “We can't hire you.” I went to the second-largest hospital system and told them I was a felon because there was no reason to hide it.

I was going to work in the morgue moving bodies because I thought, “This is great.” The hours worked where I could do calls like this, I could pitch for speaking. It was in a manner I could take time off so I could speak if I needed to travel. I'm unqualified to move bodies in a morgue because I'm a felon. When you look at those kinds of jobs and you think, “How do these men and women who get out that don't have the opportunities that I have to make it?” That's one lesson for society. I ended up as a school bus driver. I absolutely love it because I work from 5:00 until 8:30 and from 1:30 to 4:30 or 5:00.

In the middle of the day, I do things like this. Because of the way it's structured in the state of Missouri, you're all part-time. In one week, I had 106 hours. Normally I do 40, but as long as you give them two days' notice, which in speaking way more time, they'll let me have time off anytime I wanted. I'm fortuitous and it's allowed me to rebuild my life. I'm so grateful for that. It's also shown me how hard it is for society to adjust. It's almost impossible, in my opinion.

You talk about that requirement to get a job. There are a lot of people these days who are advocates for encouraging companies to consider hiring felons, especially if the job is not related to what they have been convicted of doing. This might come out the wrong way. I'm surprised that being a school bus driver was a job. I'm sure that the type of conviction was part of it. I guess different organizations have different criteria.

It's an industry thing and here's what it is. If you have a sexual crime, you couldn't do it. Home Depot in prison was one of the big names. They listed Amazon and Home Depot. I went to Home Depot but they wouldn't hire me because I was a felon. In prison, on the board, when you look for jobs, they're number two after Amazon. It's convoluted and sad. I'm not trying to be a social justice advocate, but I think you have enough audience out there that are going to say, “This is the way the world is,” because they wouldn't believe that.

You mentioned investments and other things you're doing. Do you still have that job?

No, I don't. By the way, I had gotten out of the banking business long before I was indicted. I gave a speech in 2010. I said, “Entrepreneurial banking is dead.” The government, after the 2008 crisis, has regulated it. As I say in the book, it's like going to Chick-fil-A. They want it to be a credit score and simple. That's why hedge funds and private equity are the risk-takers now. I described that years ago. That's when it happened. I said there will be entities that will come out and replace community banking or whatever name you want to put on it because the government doesn't want it anymore. They want a utility, and they're getting it.

Our guest has been Shaun Hayes. You can learn more about his book and the speaking that he does. His website is ShaunHayes.com. You talk about wanting to help people avoid the mistakes you've made. Do you do speaking for banks or financial institutions? Where are you doing your speaking?

Financial institutions, banks, and accounting firms. Ian, my former auditor, paid a $200 million fine for cheating on the CPA exam. I do a lot of universities because you like to hit kids young and young men and women. There's so much more entrepreneurial than my generation was. When you're out in that world, you don't have the checks and balances that you have in a big company. I talk a lot about a small company to instill those things. I speak mainly on Ethics. I do get a lot of requests and I did one that was a mixture of Entrepreneurship and Ethics. I was unique in the fact that I did have a successful entrepreneurial career before I committed a crime. I have fun with that too.

Shaun, thank you so much for sharing your stories in this case. I appreciate you coming on the show and talking so openly about mistakes and lessons learned along the way. I do appreciate you for being here.

Thank you for having me. I enjoy your show, Mark, and have a wonderful day.